🐯虎嗅•Freshcollected in 18m

Three forces driving the strength of the US Dollar

💡Understand how AI capital expenditure is fundamentally reshaping global finance and the US Dollar's dominance.

⚡ 30-Second TL;DR

What Changed

The Fed is shifting toward 'Fed balance sheet contraction + credit expansion' to maintain liquidity.

Why It Matters

Explains the macro-financial role of AI infrastructure investment, showing how tech spending sustains global currency dominance.

What To Do Next

Monitor AI infrastructure spending and debt issuance trends as leading indicators for capital availability in the AI sector.

Who should care:Founders & Product Leaders

Key Points

- •The Fed is shifting toward 'Fed balance sheet contraction + credit expansion' to maintain liquidity.

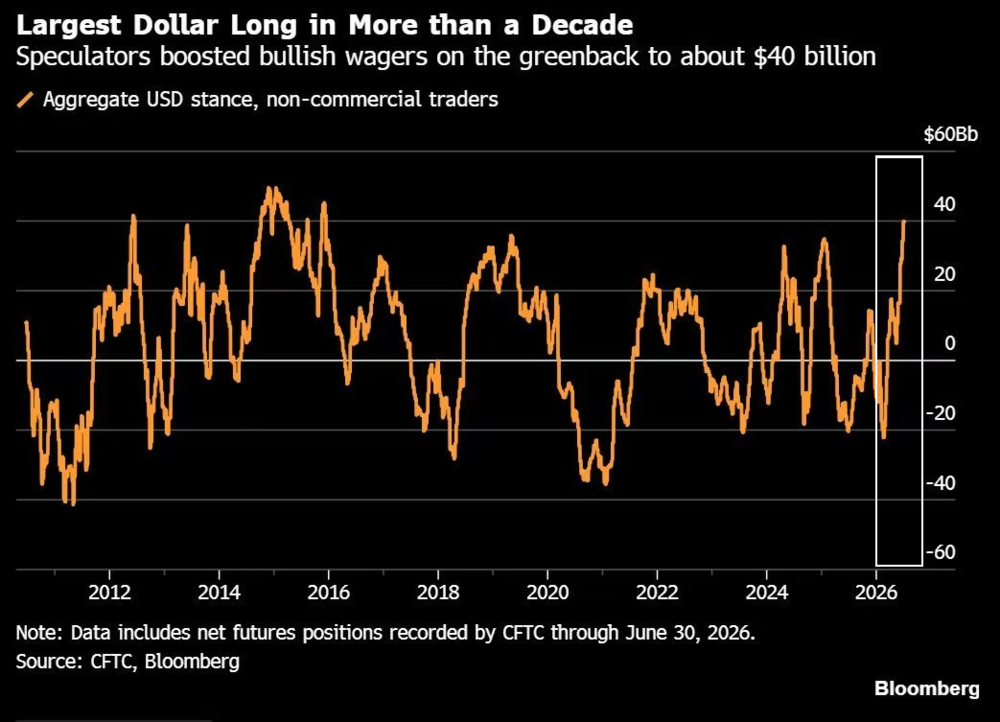

- •AI is transforming the US capital market into a global hub for AI equity and credit financing.

- •AI-related debt issuance has exceeded $600 billion since 2024, creating long-term demand for USD.

🧠 Deep Insight

AI-generated analysis for this event.

🔑 Enhanced Key Takeaways

- •The 'AI-driven capital market integration' is largely fueled by the concentration of hyperscaler capital expenditure (CapEx), which reached record levels in 2025-2026, forcing global institutional investors to reallocate portfolios toward US-listed AI infrastructure assets.

- •The US Treasury's issuance strategy has shifted to favor short-term T-bills to manage liquidity, which has inadvertently created a 'dollar trap' for foreign central banks that rely on these instruments for reserve management.

- •European economic stagnation is exacerbated by a widening 'AI productivity gap,' where the lack of a unified, high-speed capital market prevents European firms from scaling AI models at the same rate as US counterparts.

- •The Federal Reserve's 'credit expansion' mechanism is increasingly facilitated by private credit markets and non-bank financial intermediaries (NBFIs), which now account for a larger share of USD-denominated corporate lending than traditional commercial banks.

- •The surge in AI-related debt is creating a 'synthetic demand' for USD, as foreign entities must hold dollar-denominated cash reserves to service the interest payments on the massive volume of AI-infrastructure bonds issued since 2024.

🔮 Future ImplicationsAI analysis grounded in cited sources

The US Dollar will maintain its status as the primary global reserve currency through 2028.

The structural demand for USD created by AI infrastructure financing and the lack of a comparable deep-liquidity capital market in the Eurozone or China creates a high barrier to entry for alternative reserve currencies.

Global AI development will remain geographically centralized in the US.

The feedback loop between US-based AI equity markets and the ability to finance massive, dollar-denominated compute infrastructure creates a capital-moat that is difficult for other regions to replicate.

⏳ Timeline

2024-01

Initial surge in AI-related corporate debt issuance begins as hyperscalers ramp up data center investment.

2025-03

Federal Reserve signals a shift in balance sheet management to accommodate increased liquidity needs for AI-sector credit.

2026-02

US Treasury reports record-high foreign demand for short-term T-bills, signaling a flight to dollar-denominated liquidity.

📰

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: 虎嗅 ↗