🇨🇳cnBeta (Full RSS)•Stalecollected in 4h

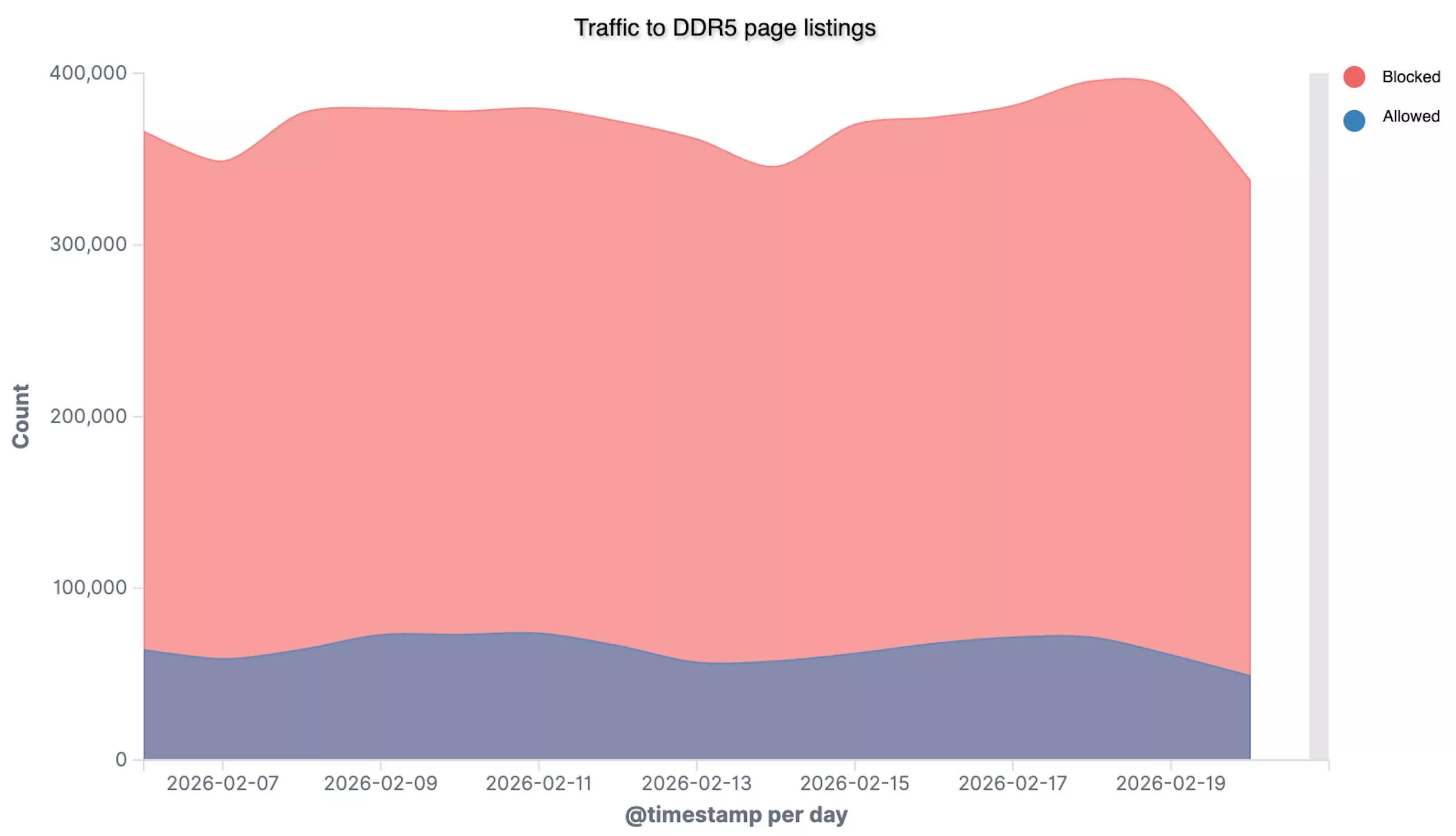

AI Data Centers Hoard Global DDR5 Supply

💡AI boom sparks DDR5 shortages—secure memory supply now.

⚡ 30-Second TL;DR

What Changed

AI data centers devouring global memory manufacturing capacity.

Why It Matters

Drives up DDR5 costs for AI training/inference setups. Practitioners face procurement delays and higher infra expenses amid AI boom.

What To Do Next

Check Micron or Samsung industrial DDR5 quotes immediately for bulk AI server builds.

Who should care:Enterprise & Security Teams

🧠 Deep Insight

Web-grounded analysis with 6 cited sources.

🔑 Enhanced Key Takeaways

- •Manufacturing capacity constraints extend beyond AI demand: The three major DRAM producers (Samsung, Micron, SK Hynix) control 90% of global supply, and new production facilities won't meaningfully increase availability until 2028, creating a multi-year structural shortage rather than a temporary disruption[4].

- •HBM production diverts standard memory: High-Bandwidth Memory manufacturing consumes three times more wafer capacity than standard DRAM, forcing producers to shift away from conventional DDR4/DDR5 chips used in consumer and automotive sectors[3].

- •Cross-sector price inflation is severe: DDR4 RAM prices surged 1,360% since April 2025, with major OEMs like Dell planning PC price increases up to 30%, while IDC forecasts a 9% PC market contraction and 5% smartphone sales decline in 2026[2][3].

- •Supply chain reallocation is permanent, not cyclical: Industry analysts describe this as a 'permanent reallocation' of supplier capacity toward AI datacenters, with data centers expected to consume 70% of all DRAM production in 2026—a structural shift fundamentally different from previous memory cycles[2][4].

- •Retail and industrial supply chains face coordinated pressure: The shortage affects the entire DDR5 ecosystem from consumer retail modules to industrial connectors and server RDIMMs, with lead times extending across all memory categories and forcing organizations to stage purchases 12-18 months in advance[1][5].

🛠️ Technical Deep Dive

- •HBM vs. Standard DRAM: HBM requires three times more wafer capacity per unit than conventional DRAM, making it resource-intensive to manufacture at scale[3].

- •DDR4 to DDR5 Migration: The transition between memory generations is creating a dual-demand scenario where legacy DDR4 systems still require supply while new platforms mandate DDR5, straining production across both standards[1][5].

- •Manufacturing Lead Times: New semiconductor manufacturing equipment requires 12-18 months or longer to install and operationalize, with orders typically placed 1-2 years in advance, making rapid capacity expansion infeasible[5].

- •Memory Module Configurations: Shortages affect specific DDR5 module sizes and preferred vendor configurations differently, forcing buyers to accept non-standard modules or pay spot market premiums[1].

🔮 Future ImplicationsAI analysis grounded in cited sources

Memory shortage will persist through 2027 despite new manufacturing capacity announcements

Industry analysts project that expanded production facilities will not materially impact global supply until 2028, with major producers already selling 2027-2028 capacity commitments[4].

Consumer PC market will shift toward cloud-based computing models as hardware costs become prohibitive

Sustained DDR5 price inflation and hardware shortages may accelerate adoption of subscription-based cloud computing over local PC ownership[4].

Automotive and IoT sectors will face extended supply constraints as datacenter demand absorbs high-performance memory capacity

The permanent reallocation of manufacturing toward AI infrastructure means conventional DRAM applications will remain supply-constrained even as new capacity comes online[3].

⏳ Timeline

2025-04

DDR4 RAM prices begin dramatic surge, increasing 1,360% by March 2026

2025-10

Micron announces discontinuation of Crucial consumer brand to focus entirely on AI market supply

2025-12

IDC updates 2026 forecasts: 9% PC market decline and 5% smartphone sales decline due to memory pricing

2026-01

Dell announces up to 30% PC price increases attributed to RAM shortage

2026-02

Industry analysts confirm memory shortage as worst in history with three core suppliers unable to meet demand

2026-03

Data centers consuming 70% of global DRAM production; supply-demand imbalance reaches critical levels

📎 Sources (6)

Factual claims are grounded in the sources below. Forward-looking analysis is AI-generated interpretation.

- catalystdatasolutionsinc.com — Ddr5 Memory Shortage 2026

- Tom's Hardware — Data Centers Will Consume 70 Percent of Memory Chips Made in 2026 Supply Shortfall Will Cause the Chip Shortage to Spread to Other Segments

- enkiai.com — AI Memory Crisis 2026 Unpacking the Global Shortage

- windowscentral.com — Memory Shortage 2026 Tech AI Datacenters

- networkworld.com — Whats Causing the Memory Shortage

- msi.com — Memory Shortage 2025 2026 Causes Impact and How to Build a Pc

📰

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: cnBeta (Full RSS) ↗