💰钛媒体•Stalecollected in 81m

High-Level ADAS: Auto Market's Post-Price War Anchor?

💡Price wars fail: Is ADAS the auto AI growth pivot? China market insights

⚡ 30-Second TL;DR

What Changed

Price wars diminishing in auto sector

Why It Matters

Shifts auto competition to AI-driven features, boosting demand for ADAS tech stacks.

What To Do Next

Benchmark Huawei or XPeng L3 ADAS APIs for integration feasibility.

Who should care:Enterprise & Security Teams

🧠 Deep Insight

Web-grounded analysis with 4 cited sources.

🔑 Enhanced Key Takeaways

- •Chinese automakers are shifting competition from price-based strategies to advanced autonomous driving capabilities, with BYD and emerging EV leaders leveraging intelligent driving systems as differentiation tools as regulatory price controls take effect[1][2]

- •The phase-out of EV subsidies and trade-in incentives in 2026 is forcing OEMs to develop higher-margin, technology-driven products rather than compete on cost, fundamentally reshaping the competitive landscape[3]

- •NEV (New Energy Vehicle) sales now represent 50% of China's auto market as of end-2025, with 100% of net growth coming from electrification, making advanced ADAS a critical feature for market participation rather than a luxury differentiator[4]

🔮 Future ImplicationsAI analysis grounded in cited sources

ADAS adoption will accelerate as price competition regulation tightens

Foreign luxury brands face accelerating market share erosion without rapid ADAS integration

Consolidation will intensify among Chinese automakers lacking ADAS capabilities

The shift from quantity to quality competition, combined with depleted government incentives, will eliminate smaller players unable to invest in autonomous driving technology[3]

⏳ Timeline

2024-02

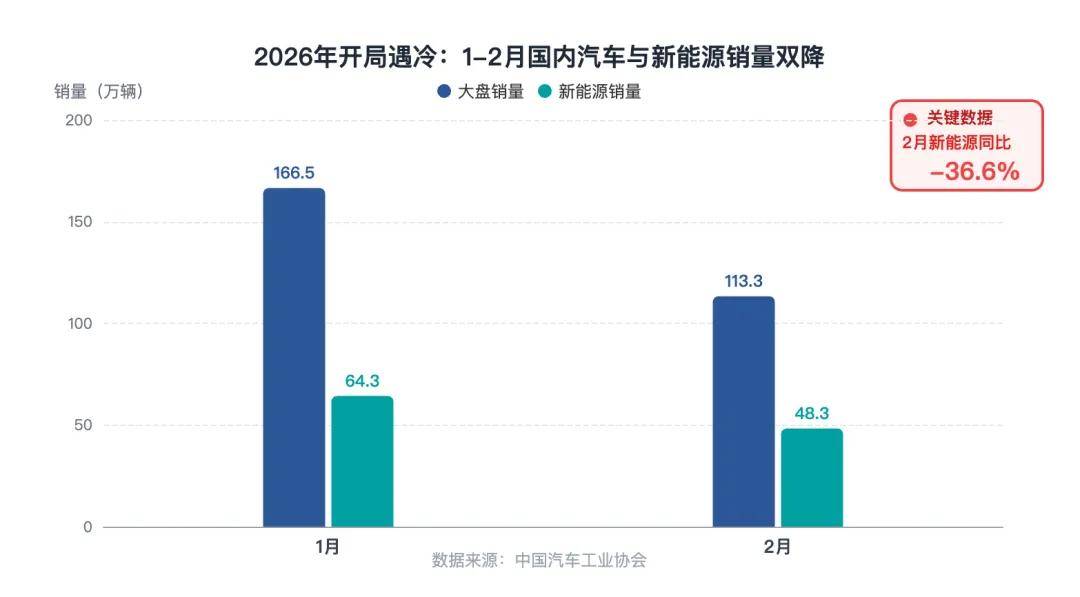

Passenger car sales decline reaches fastest pace in nearly two years, signaling price war severity

2025-12

NEV sales reach 50% market share parity with ICE vehicles; EV subsidies and trade-in incentives phase out

2026-02

State Administration for Market Regulation releases guidelines banning below-cost pricing; enforcement begins

📎 Sources (4)

Factual claims are grounded in the sources below. Forward-looking analysis is AI-generated interpretation.

📰

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: 钛媒体 ↗