💰钛媒体•較早收集於 15m

國產AI晶片崛起:三大門派、瓜分英偉達

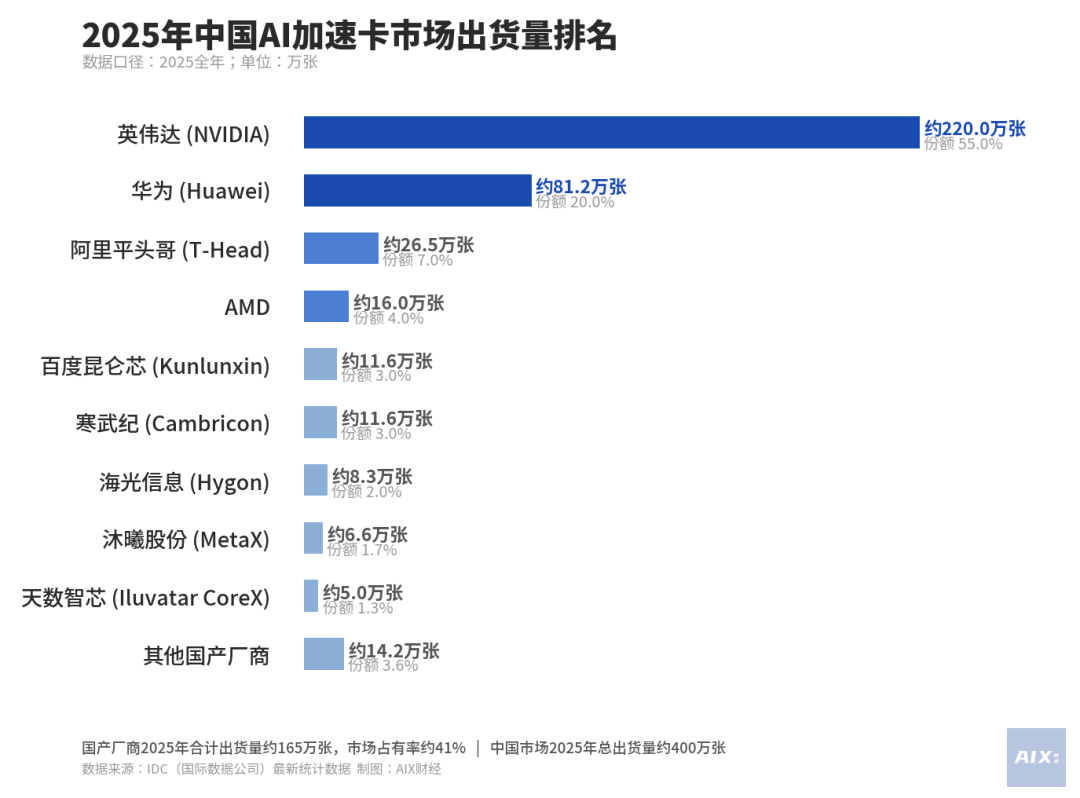

💡中國晶片門派瓜分英偉達份額—硬體多元化關鍵。

⚡ 30-Second TL;DR

有什麼變化

三大中國AI晶片門派獲得青睞

為什麼重要

加劇全球AI晶片競爭,可能降低成本並緩解供應鏈風險,利於非美國主導的AI部署。

下一步行動

基準測試中國三大AI晶片門派晶片對比Nvidia H100的推理效率。

誰應關注:Enterprise & Security Teams

關鍵要點

- •三大中國AI晶片門派獲得青睞

- •直接挑戰英偉達市場主導地位

- •國產替代品削弱英偉達無敵地位

🧠 深度解析

AI-generated analysis for this event.

🔑 增強重點摘要

- •The three factions are categorized by their origin: tech giants (e.g., Huawei/Ascend), specialized AI chip startups (e.g., Biren Technology, Moore Threads), and state-backed research institutes, each targeting different segments of the training and inference market.

- •US export controls on high-end GPUs like the H100 and A100 have acted as a catalyst, forcing Chinese cloud providers and enterprises to adopt domestic silicon to ensure supply chain continuity.

- •Software ecosystem maturity remains the primary bottleneck; while hardware performance is closing the gap, Chinese manufacturers are heavily investing in proprietary software stacks to improve compatibility with PyTorch and TensorFlow.

📊 競品分析▸ Show

| Feature | Nvidia H20 (China-specific) | Huawei Ascend 910B | Biren BR100 |

|---|---|---|---|

| Architecture | Hopper (Cut-down) | Da Vinci | Big Island |

| FP16/BF16 TFLOPS | ~148 | ~320 | ~512 |

| Memory Bandwidth | 900 GB/s | 1.2 TB/s | 2 TB/s |

| Software Stack | CUDA | CANN | BIRENSUPA |

🛠️ 技術深入

- •Huawei Ascend 910B utilizes a 7nm process node and is optimized for large-scale cluster training, supporting high-speed interconnects (HCCS) to rival NVLink.

- •Biren Technology's BR100 employs a chiplet architecture, allowing for higher yields and scalability in high-performance computing (HPC) workloads.

- •Most domestic chips are shifting focus from pure raw compute to high-bandwidth memory (HBM) integration to mitigate the memory wall bottleneck in LLM training.

- •Development of 'CANN' (Compute Architecture for Neural Networks) by Huawei serves as the direct alternative to CUDA, providing a library of operators specifically tuned for Ascend hardware.

🔮 前景展望AI analysis grounded in cited sources

Domestic market share for AI training chips in China will exceed 40% by 2027.

Increasingly stringent US export restrictions are compelling domestic firms to prioritize local procurement regardless of initial performance gaps.

Nvidia will lose its monopoly on the Chinese LLM training market.

The rapid maturation of domestic software stacks like CANN is lowering the switching costs for Chinese AI labs.

⏳ 時間線

2022-08

US government imposes initial restrictions on the export of high-end AI chips to China.

2023-10

US expands export controls, effectively banning the sale of Nvidia's A800 and H800 chips to China.

2024-03

Huawei reports significant scaling of Ascend 910B production to meet domestic demand.

2025-06

Major Chinese cloud providers announce large-scale migration of inference workloads to domestic chip architectures.

📰

AI 週報

閱讀本週精選 AI 大事摘要 →

👉相關動態

AI 策展新聞聚合。所有內容版權歸原始發布者所有。

原始來源: 钛媒体 ↗