Rising Memory Costs Force Smartphone RAM Regression

💡Hardware memory constraints are tightening; learn how this impacts the deployment of on-device AI models.

⚡ 30-Second TL;DR

What Changed

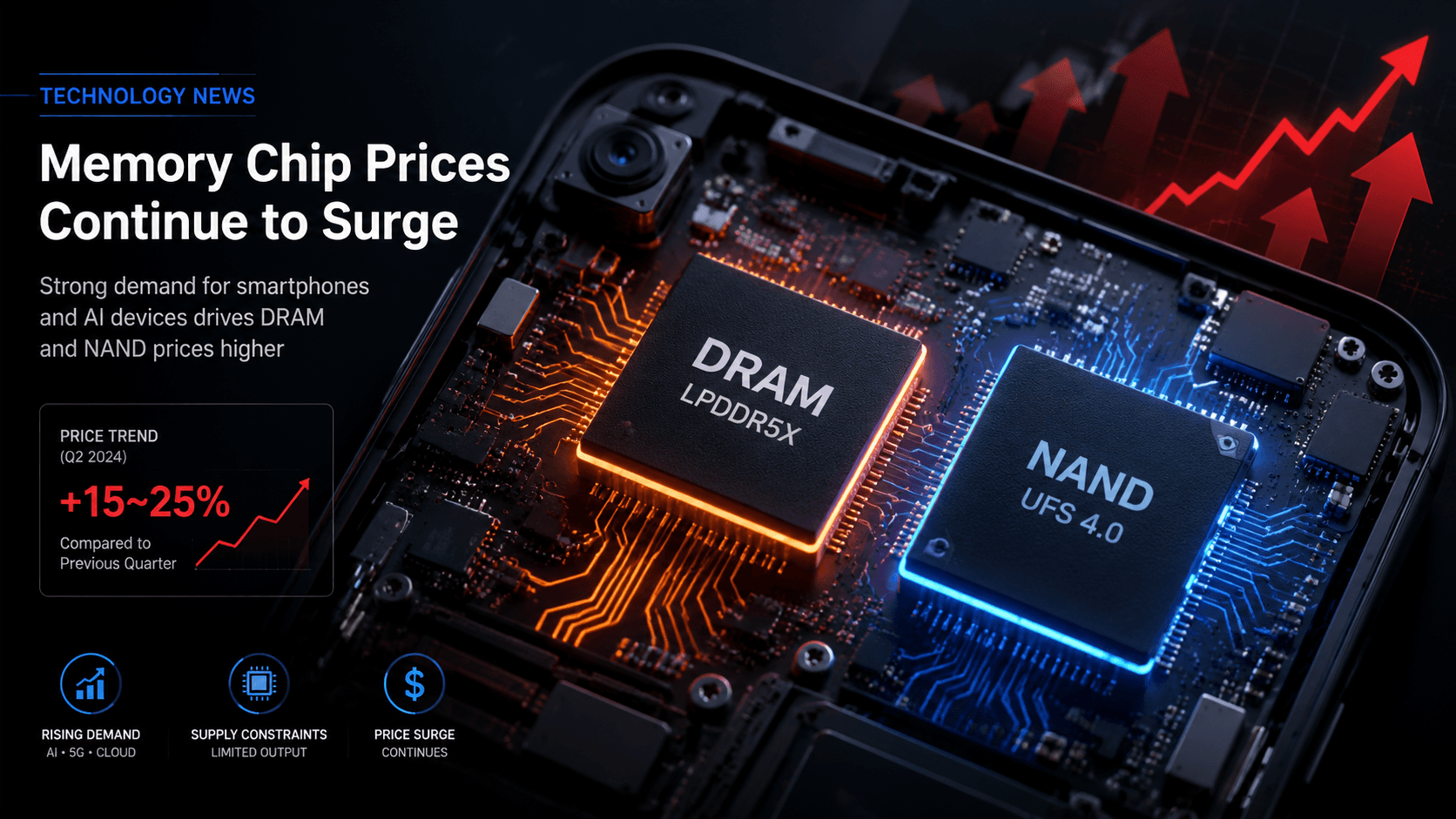

DRAM and NAND flash prices are significantly increasing.

Why It Matters

Reduced RAM in entry-level devices will limit the performance of on-device AI features, potentially slowing the adoption of local LLMs in budget smartphones.

What To Do Next

Optimize your mobile AI models for 6GB RAM constraints to ensure compatibility with the next generation of budget devices.

Key Points

- •DRAM and NAND flash prices are significantly increasing.

- •Entry-level smartphone RAM is regressing from 12GB to 6GB.

- •Hardware cost pressures are impacting consumer-facing device specifications.

🧠 Deep Insight

Web-grounded analysis with 24 cited sources.

🔑 Enhanced Key Takeaways

- •The primary driver for the surging memory prices is the explosive demand from AI data centers for high-bandwidth memory (HBM) and server-grade DRAM, leading to a strategic reallocation of manufacturing capacity away from consumer-grade memory.

- •Memory costs now account for a significantly larger portion of the Bill of Materials (BOM) for entry-level smartphones, surging from under 10% to over 40% in some cases, making sub-$150 smartphones potentially uneconomical to produce.

- •The memory price surge is not a temporary market correction but a structural supply crunch, with new production capacity not expected until 2027, implying elevated component costs for at least two years.

- •Global smartphone shipments are projected to decline significantly in 2026 (e.g., 8.4% by Gartner, 13.9% by Counterpoint), marking the steepest contraction in over a decade, as manufacturers struggle with costs and consumers delay upgrades.

- •Chinese smartphone manufacturers like Xiaomi and Transsion have already slashed their 2026 shipment targets by tens of millions of units due to the memory crunch, indicating direct operational consequences.

🛠️ Technical Deep Dive

- DRAM (Dynamic Random-Access Memory):

- LPDDR6, the next-generation standard, is expected to achieve data rates up to 14.4 Gbps, representing a 50% improvement over LPDDR5X speeds.

- LPDDR6 features a x24 data bus per device, organized into two x12 sub-channels, making it the first DRAM with a non-power-of-2 data width. It also integrates metadata directly into data packets, reducing the need for dedicated pins.

- Enhanced power management in LPDDR6 includes dual-rail approaches (around 1.0 V and 0.875 V) and more Dynamic Voltage Frequency Scaling operating points, targeting 20-30% lower operating power compared to LPDDR5X.

- The production of High Bandwidth Memory (HBM) for AI applications strategically displaces conventional DRAM, with one HBM wafer potentially displacing three standard DDR5 wafers due to larger die sizes and increased complexity.

- NAND Flash:

- 3D NAND technology is advancing with manufacturers pushing beyond 200 layers, such as Samsung's 9th-generation V-NAND and Micron's 276-layer QLC NAND, leading to significant areal density improvements and lower cost-per-bit.

- Quad-Level Cell (QLC) NAND, which stores four bits per cell, offers the lowest cost per gigabyte among mainstream NAND architectures, typically 15-25% below equivalent TLC solutions. It is increasingly adopted in enterprise SSDs for archival and AI training datasets, reducing cost per terabyte by nearly 20% compared to TLC.

- The evolution towards higher-layer 3D NAND and QLC/PLC (Penta-Level Cell) architectures aims to enhance storage density and reduce cost per bit, making these solutions more competitive for mass data storage.

🔮 Future ImplicationsAI analysis grounded in cited sources

⏳ Timeline

📎 Sources (24)

Factual claims are grounded in the sources below. Forward-looking analysis is AI-generated interpretation.

- unibetter-ic.com

- avnet.com

- procurementpro.com

- enkiai.com

- jakelectronics.com

- indianexpress.com

- itbrief.co.uk

- vietnamnet.vn

- counterpointresearch.com

- gadgethacks.com

- gartner.com

- electronicsforyou.biz

- scmp.com

- synopsys.com

- biwintechnology.com

- cadence.com

- keysight.com

- techinsights.com

- dataintelo.com

- globalinsightservices.com

- congruencemarketinsights.com

- gminsights.com

- versalogic.com

- elinfor.com

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: Pandaily ↗