Nvidia Q4 Earnings Beat, Growth Unpeaked

💡Nvidia Q4 crushes estimates; Huang sees endless AI chip demand ahead

⚡ 30-Second TL;DR

What Changed

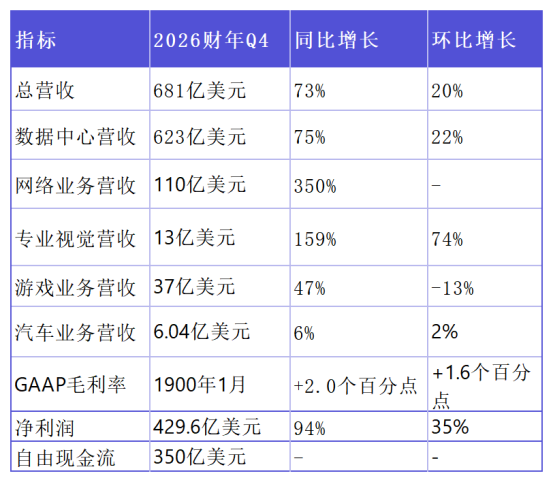

Q4 financial results exceeded market expectations

Why It Matters

Bolsters Nvidia's AI chip leadership, influencing procurement decisions for data centers and AI training.

What To Do Next

Review Nvidia's Q4 guidance and stock up on H100/H200 for AI workloads.

🧠 Deep Insight

Web-grounded analysis with 7 cited sources.

🔑 Enhanced Key Takeaways

- •NVIDIA's Data Center revenue reached $193.7 billion for fiscal 2026, representing 68% year-over-year growth and comprising 89.8% of total company revenue, demonstrating extreme concentration in accelerated computing and AI infrastructure.

- •The company unveiled the NVIDIA Rubin platform with six new chips designed to reduce inference token costs by up to 10x compared to Blackwell, signaling a strategic shift toward cost optimization as a competitive advantage in the AI infrastructure market.

- •NVIDIA returned $41.1 billion to shareholders during fiscal 2026 through buybacks and dividends while maintaining record capital expenditure investments, indicating confidence in sustained demand and financial flexibility despite gross margin compression from 75.0% to 71.1% year-over-year.

📊 Competitor Analysis▸ Show

| Metric | NVIDIA (Q4 FY26) | Context |

|---|---|---|

| Q4 Revenue | $68.1B | Record quarterly result |

| Data Center Revenue (FY26) | $193.7B | 68% YoY growth |

| Gross Margin | 71.1% | Down 3.9 pts YoY |

| Operating Income (FY26) | $130.4B | Up 60% YoY |

| EPS (Q4 GAAP) | $1.76 | Up 98% YoY |

Note: Search results contain no direct competitor financial comparisons (AMD, Intel, custom silicon providers). Competitor analysis cannot be reliably constructed from provided sources.

🛠️ Technical Deep Dive

- NVIDIA Rubin Platform: Six-chip architecture designed for inference optimization with up to 10x reduction in inference token cost versus Blackwell generation

- Blackwell GPU: Powers current data center dominance; deployed across AWS, Google Cloud, Microsoft Azure, and Oracle Cloud Infrastructure

- DLSS 4.5: AI-powered graphics technology delivering advances in rendering quality for gaming and professional visualization

- RTX PRO 5000 72GB: Blackwell-based GPU for large model training and agentic AI workflows in professional visualization segment

- DGX Spark: System optimized for open-source AI models with performance improvements in fiscal 2026

🔮 Future ImplicationsAI analysis grounded in cited sources

⏳ Timeline

📎 Sources (7)

Factual claims are grounded in the sources below. Forward-looking analysis is AI-generated interpretation.

- stocktitan.net — Nvidia Announces Financial Results for Fourth Quarter and Fiscal J0kg9vc0geqr

- fortune.com — Nvidia Nvda Earnings Q4 Results Jensen Huang

- nvidianews.nvidia.com — Nvidia Announces Financial Results for Fourth Quarter and Fiscal 2025

- nvidianews.nvidia.com — Nvidia Announces Financial Results for Fourth Quarter and Fiscal 2026

- investor.nvidia.com — Default

- investor.nvidia.com — Default

- investor.nvidia.com — Default

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: 钛媒体 ↗