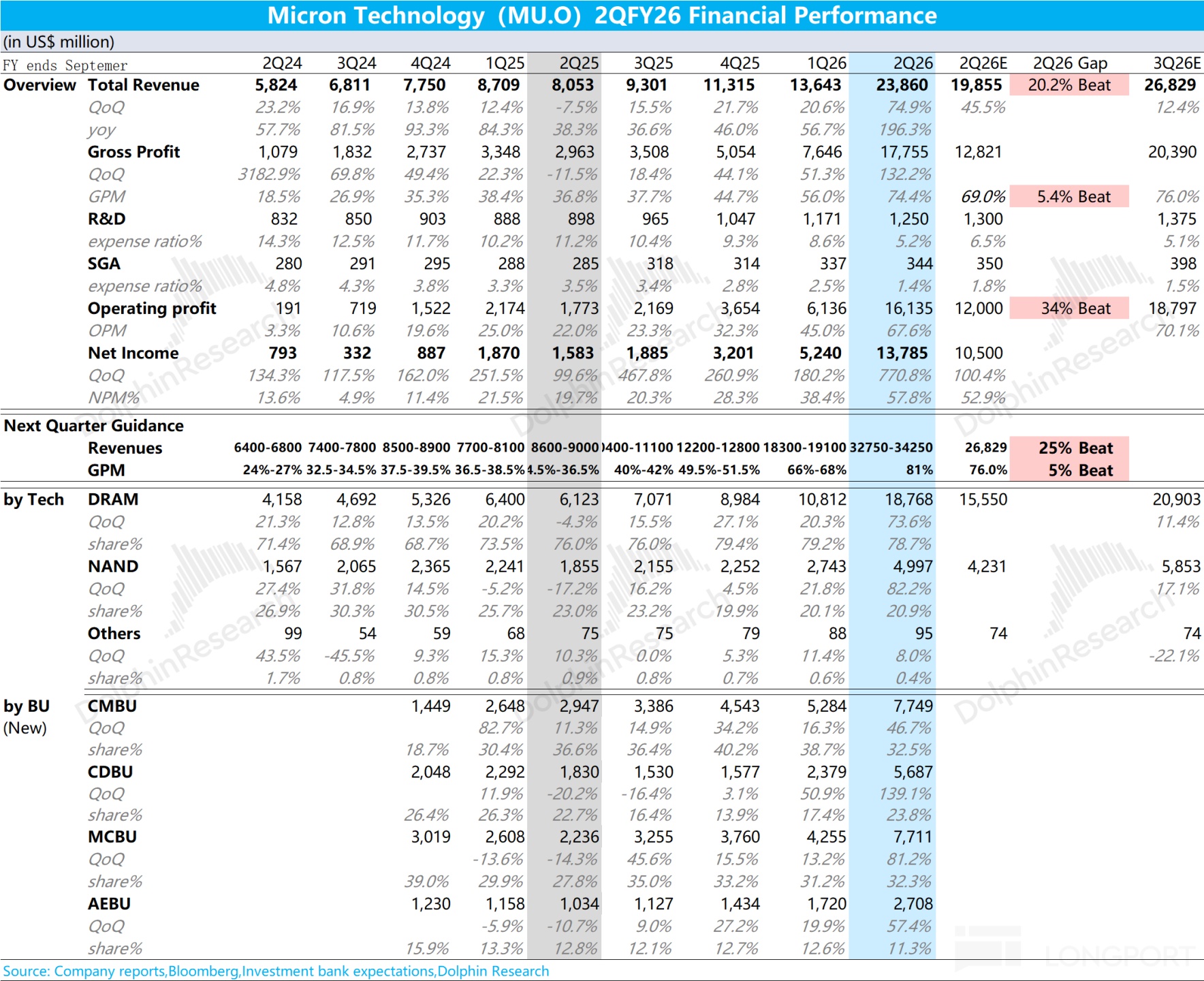

Micron Storage Booms on AI Demand

💡AI drives Micron's storage price surge – critical for planning infra costs and supply.

⚡ 30-Second TL;DR

What Changed

AI accelerates explosive storage demand growth

Why It Matters

Rising storage prices signal robust AI infrastructure demand, which could elevate costs for training large models but stabilize supply chains long-term. AI practitioners may face higher memory expenses yet benefit from innovation push.

What To Do Next

Benchmark Micron HBM3E pricing for your AI data center memory procurement.

🧠 Deep Insight

Web-grounded analysis with 7 cited sources.

🔑 Enhanced Key Takeaways

- •Micron's HBM (High-Bandwidth Memory) capacity is fully sold out through 2026 under binding contracts, providing unprecedented revenue visibility for a traditionally cyclical memory business[3].

- •The company has shifted its business model from commodity 'bit' sales to integrated 'solutions' with advanced packaging, capturing a higher percentage of the value chain than fabless competitors[6].

- •Micron holds approximately 21% market share in HBM but is growing fastest, with HBM3E noted as the most power-efficient option on the market, positioning it ahead of Samsung in the current cycle[6][7].

- •LPDDR memory adoption is accelerating dramatically, with systems expected to ship in 2026 containing triple the LPDDR content compared to 2025, reducing time to first token by 98% for AI inference[1].

- •The memory industry's structural shift to three-tier architecture (HBM, SOCAMM, DDR5) and long-term contracts has transformed Micron from a cyclical commodity supplier into a critical AI infrastructure essential[2].

📊 Competitor Analysis▸ Show

| Competitor | HBM Market Share | Key Advantage | Current Position |

|---|---|---|---|

| SK Hynix | ~55% | Mass Reflow Molded Underfill (MR-MUF) thermal management for ultra-dense 16-high stacks | Overall HBM market leader[6] |

| Micron | ~21% | Most power-efficient HBM3E; fastest growth rate | Preferred by Tier-1 AI customers; fully booked 2026 capacity[6][7] |

| Samsung Electronics | Unspecified | Hybrid Bonding technology for HBM4 | Lagged in HBM3E qualifications throughout 2025; long-term threat[6] |

🛠️ Technical Deep Dive

- •HBM4 specifications: 11.7 Gbps performance with pre-sold 2026 capacity, delivering superior power efficiency and yield compared to competitors[2].

- •SOCAMM2 module: 256GB capacity modules announced March 3, 2026, doubling capacity within the same power envelope and enabling up to 2TB of memory per server CPU for inference tasks requiring million-token-long contexts[2].

- •LPDDR optimization: Systems shipping in 2026 with triple the LPDDR content versus 2025, reducing inference time-to-first-token by 98% and significantly improving inference performance[1].

- •Three-tier memory architecture: HBM for compute-intensive tasks, SOCAMM for mid-tier workloads, and DDR5 for standard operations, with Micron co-designing 'Vera Rubin' platform with NVIDIA[2].

- •Manufacturing integration: Micron owns the entire manufacturing process from wafer fabrication through advanced assembly and testing, capturing higher value chain percentage than fabless competitors[6].

🔮 Future ImplicationsAI analysis grounded in cited sources

⏳ Timeline

📎 Sources (7)

Factual claims are grounded in the sources below. Forward-looking analysis is AI-generated interpretation.

- marketbeat.com — Micron Technology Says AI Memory Demand Still Outstrips Supply Through 2026 Hbm4 Shipping Early 2026 02 14

- ainvest.com — Micron Technology Mu Deep Dive 2026 Storage Anchor AI Infrastructure Era 2603

- alphaspread.com — Micron Rallies As AI Demand Sells Out 2026 Hbm Production Strong Q1 Results and Analyst Upgrades Fuel Optimism

- indexbox.io — Micron Technologys AI Driven Market Surge and Memory Price Outlook

- youtube.com — Watch

- markets.financialcontent.com — Finterra 2026 3 13 Microns AI Supercycle Why 2026 Is the Year of the Memory Fortress

- moneymorning.com — Micron the Overlooked Powerhouse in AI Memory

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: 钛媒体 ↗