Memory Price Surge Forces Smartphone Spec Downgrades

💡Hardware memory constraints are the new bottleneck for on-device AI; learn how to optimize for lower RAM.

⚡ 30-Second TL;DR

What Changed

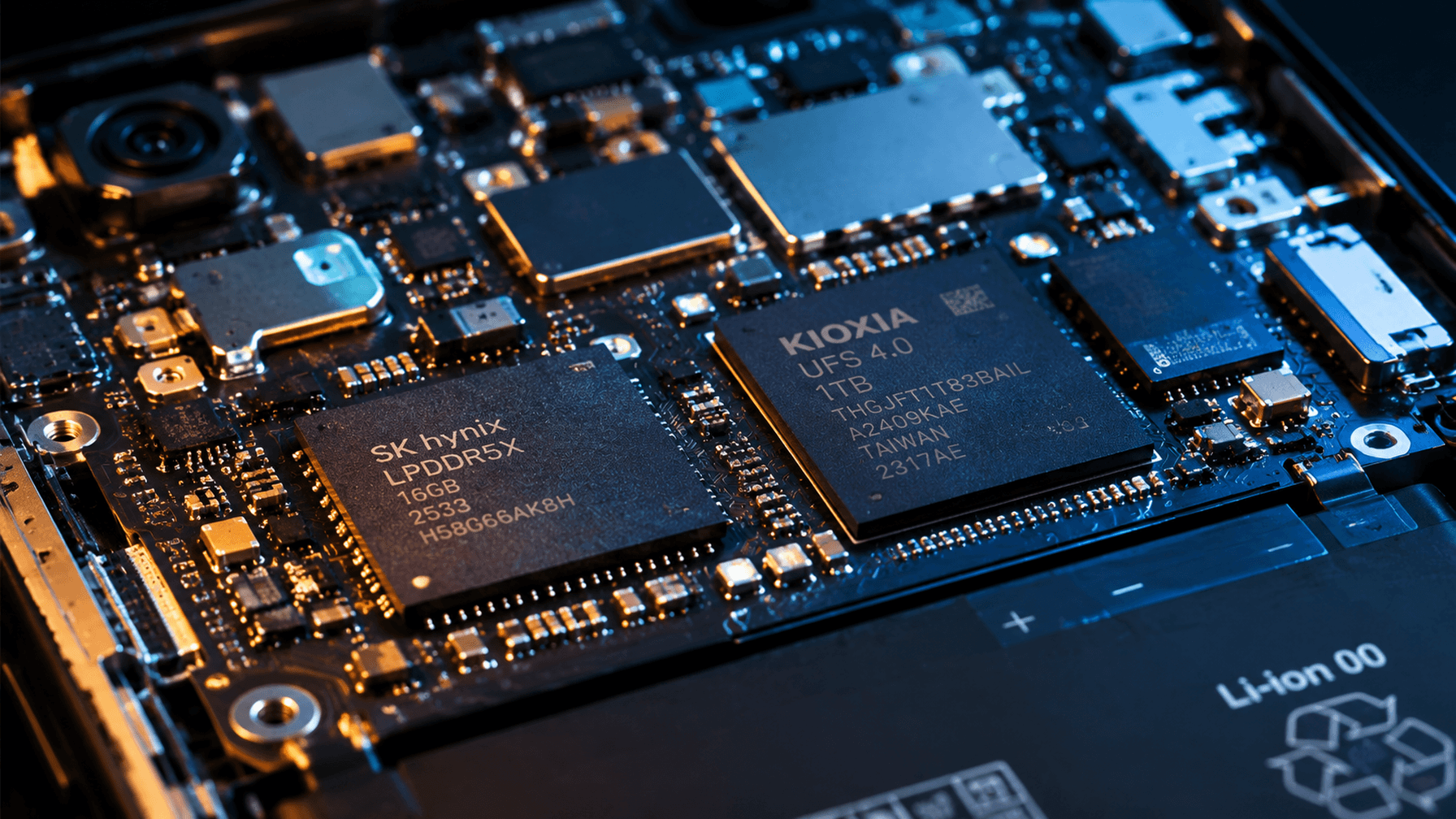

DRAM and NAND memory prices are experiencing a significant surge.

Why It Matters

The increased cost of memory will likely slow down the adoption of on-device AI, which requires significant RAM to run local LLMs efficiently. Developers should optimize models for lower memory footprints to maintain performance on budget devices.

What To Do Next

Optimize your local LLM inference pipelines using 4-bit or 8-bit quantization to ensure compatibility with 6GB RAM constraints.

Key Points

- •DRAM and NAND memory prices are experiencing a significant surge.

- •Smartphone manufacturers are downgrading entry-level RAM from 12GB to 6GB.

- •Xiaomi's Lei Jun predicts the price rally may last for two years.

- •Hardware cost increases are directly impacting consumer device specifications.

🧠 Deep Insight

Web-grounded analysis with 29 cited sources.

🔑 Enhanced Key Takeaways

- •The primary driver behind the current memory price surge is the unprecedented demand from AI data centers for high-end memory, specifically High-Bandwidth Memory (HBM) and enterprise SSDs, which are consuming a significant portion of global memory supply.

- •Memory manufacturers are strategically reallocating their production capacity from conventional consumer-grade DRAM and NAND to these higher-margin AI-centric products, leading to a structural shortage for devices like smartphones and PCs.

- •The price increases have been substantial, with DRAM contract prices rising by 55-95% quarter-over-quarter (QoQ) and NAND flash prices jumping by 33-75% QoQ in Q1 and Q2 2026, marking an unprecedented convergence of record highs across all memory categories.

- •This memory market has entered a multi-year 'supercycle' driven by AI, with industry analysts and memory vendors predicting that shortages and elevated prices will persist through at least 2027 and potentially into 2028.

- •The impact of rising memory costs extends beyond just RAM configurations, forcing budget smartphone makers to also revert to older display technologies like 1080p LCD panels and notch designs, and increasing the overall Bill of Materials (BOM) costs for all smartphone segments.

🛠️ Technical Deep Dive

- DRAM (Dynamic Random Access Memory) cells are fundamental units of data storage, each comprising a transistor and a capacitor, manufactured through intricate processes requiring nanometer-scale precision.

- NAND flash memory utilizes 3D structures (e.g., 3D NAND) and Triple-Level Cell (TLC) technology to achieve higher storage density and a lower cost per bit, with 3D structures expected to account for 69.8% of the market in 2026.

- High-Bandwidth Memory (HBM) is a specialized form of DRAM designed for high-performance computing and AI accelerators, consuming approximately three times more wafer area per gigabyte compared to standard DRAM, and requiring advanced packaging.

- The shift in manufacturing capacity towards HBM directly reduces the available wafer capacity for conventional DRAM used in consumer devices.

- DDR5 is experiencing widespread adoption, and high-capacity RDIMMs are a primary procurement target for North American cloud service providers deploying AI inference infrastructure.

🔮 Future ImplicationsAI analysis grounded in cited sources

⏳ Timeline

📎 Sources (29)

Factual claims are grounded in the sources below. Forward-looking analysis is AI-generated interpretation.

- avnet.com

- ampheo.com

- gotraka.com

- weareconker.com

- greennode.ai

- idc.com

- hbs.net

- unibetter-ic.com

- biggo.com

- suntsu.com

- techyultra.com

- fool.com

- pandaily.com

- elinfor.com

- nand-research.com

- informa.com

- counterpointresearch.com

- counterpointresearch.com

- versalogic.com

- medium.com

- medium.com

- 36kr.com

- thermofisher.com

- coherentmarketinsights.com

- sourceability.com

- smc-cloud.com

- androidauthority.com

- techradar.com

- latestly.com

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: Pandaily ↗