💰钛媒体•Stalecollected in 8m

LiDAR Profits Surge as Carmakers Struggle

💡LiDAR boom signals profitable AV infra play for robotics AI builders

⚡ 30-Second TL;DR

What Changed

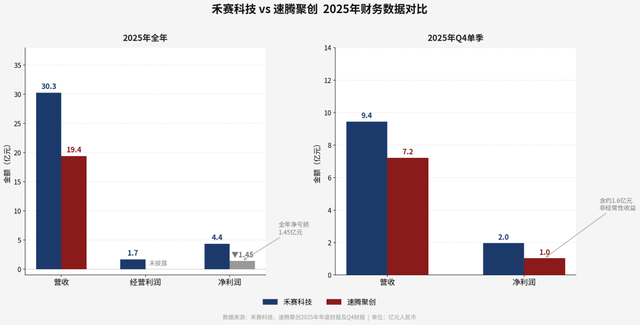

Carmakers face losses in competitive EV market

Why It Matters

Highlights shift in AV value chain towards sensors, urging investors to favor LiDAR over full vehicle assembly.

What To Do Next

Benchmark Hesai and RoboSense LiDAR specs for your AV perception stack integration.

Who should care:Founders & Product Leaders

Key Points

- •Carmakers face losses in competitive EV market

- •LiDAR suppliers like Hesai achieve strong profitability

- •Hesai strategy emphasizes profit protection

- •RoboSense focuses on rapid scale expansion

🧠 Deep Insight

AI-generated analysis for this event.

🔑 Enhanced Key Takeaways

- •Hesai has successfully transitioned its business model toward high-margin, software-defined LiDAR solutions, leveraging proprietary ASIC chipsets to reduce unit costs while maintaining premium pricing in the luxury EV segment.

- •RoboSense's strategy of aggressive market share acquisition is heavily subsidized by strategic partnerships with major Chinese OEMs, prioritizing volume-based manufacturing efficiencies over immediate bottom-line profitability.

- •The divergence in financial performance is exacerbated by the 'price war' in the Chinese EV market, forcing carmakers to squeeze Tier-1 suppliers, which has led to a market consolidation where only LiDAR vendors with strong vertical integration can sustain operations.

📊 Competitor Analysis▸ Show

| Feature | Hesai (AT128/AT512) | RoboSense (M1/M3) | Innovusion (Falcon) |

|---|---|---|---|

| Primary Strategy | High-margin/Premium | Volume/Market Share | OEM-specific integration |

| Core Tech | Proprietary ASIC | Hybrid Solid-State | Fiber Laser/Galvo |

| Pricing Focus | Value-based pricing | Cost-leadership | Project-based pricing |

| Market Position | Global leader in revenue | Leader in shipment volume | Strong in high-speed ADAS |

🛠️ Technical Deep Dive

- •Hesai utilizes a 'Vela' and 'AT' series architecture, heavily reliant on in-house developed ASIC chips that integrate signal processing and data acquisition, significantly reducing component count and power consumption.

- •RoboSense employs a modular 'M-Platform' design, which allows for rapid iteration and manufacturing scalability by utilizing a standardized optical path design that can be adapted for different range requirements.

- •Both companies are shifting from 905nm to 1550nm laser wavelengths for long-range detection, though 905nm remains the dominant choice for mass-market ADAS due to lower cost of components.

🔮 Future ImplicationsAI analysis grounded in cited sources

LiDAR industry will undergo significant M&A activity by 2027.

The inability of smaller, non-vertically integrated LiDAR startups to compete with the scale and margin-protection strategies of Hesai and RoboSense will force consolidation.

Average Selling Price (ASP) of automotive LiDAR will drop below $300 by 2027.

Intense competition for OEM design wins is driving a race to the bottom in pricing, necessitating further manufacturing automation and chip-level integration.

⏳ Timeline

2023-02

Hesai Group completes its IPO on the Nasdaq, becoming the first Chinese LiDAR company to list in the US.

2024-01

RoboSense officially lists on the Hong Kong Stock Exchange, focusing on rapid production scaling.

2025-06

Hesai reports its first consecutive quarters of positive operating cash flow, signaling a shift to profitability.

📰

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: 钛媒体 ↗