💰钛媒体•Freshcollected in 2m

AI payment adoption faces market challenges

💡Learn why AI-driven payment solutions are struggling to gain traction in the current market.

⚡ 30-Second TL;DR

What Changed

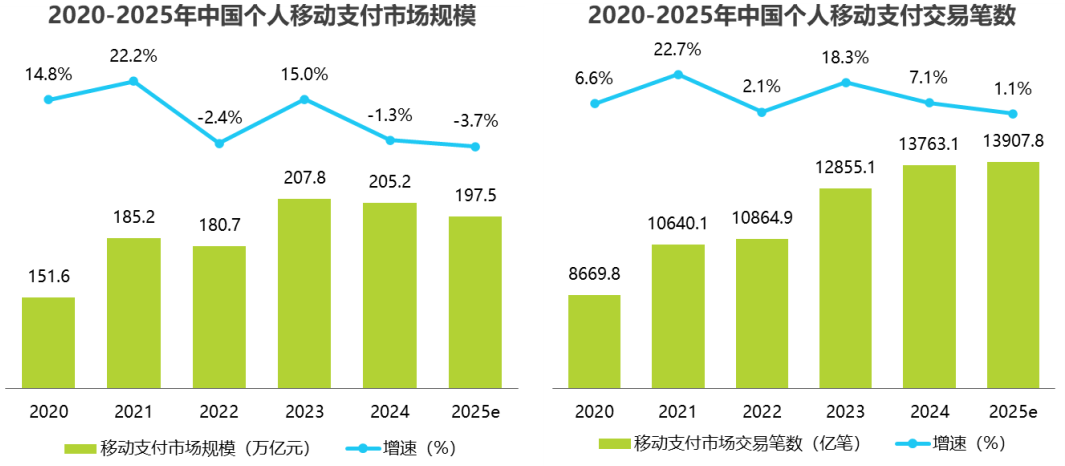

AI payment market lacks explosive growth

Why It Matters

Highlights the difficulty of integrating AI into mature financial infrastructure.

What To Do Next

Evaluate the specific UX friction points in your AI-driven fintech product before scaling.

Who should care:Founders & Product Leaders

Key Points

- •AI payment market lacks explosive growth

- •Major tech companies struggling with adoption

- •Expectations vs. reality gap in fintech

🧠 Deep Insight

AI-generated analysis for this event.

🔑 Enhanced Key Takeaways

- •Regulatory scrutiny regarding data privacy and AI-driven credit scoring has created significant friction for fintech firms attempting to automate payment approvals.

- •Interoperability issues between legacy banking infrastructure and modern AI payment layers remain a primary bottleneck for large-scale enterprise deployment.

- •Consumer trust remains a critical barrier, with surveys indicating a preference for traditional authentication methods over AI-based biometric or behavioral payment verification.

- •The high computational cost of running real-time fraud detection models at scale is eroding the profit margins of AI-integrated payment processors.

- •Market saturation in digital wallet services has forced AI payment providers to pivot toward niche B2B cross-border settlement solutions rather than consumer-facing retail payments.

📊 Competitor Analysis▸ Show

| Feature | AI-Integrated Payment Processors | Traditional Payment Gateways | Decentralized Finance (DeFi) Protocols |

|---|---|---|---|

| Fraud Detection | Real-time ML/Behavioral | Rule-based/Static | Consensus-based/On-chain |

| Transaction Speed | High (Latency dependent) | Moderate | Variable (Network dependent) |

| Implementation Cost | High (API/Integration) | Low (Standardized) | Moderate (Gas/Smart Contract) |

| Regulatory Risk | High (Black-box AI) | Low (Established) | Very High (Uncertain) |

🛠️ Technical Deep Dive

- Implementation typically relies on Transformer-based architectures for analyzing transaction sequences to detect anomalies in real-time.

- Integration often utilizes Federated Learning frameworks to train fraud detection models across decentralized datasets without compromising user privacy.

- API layers frequently employ Graph Neural Networks (GNNs) to map complex relationships between entities, accounts, and IP addresses to identify money laundering patterns.

- Edge computing is increasingly used to process biometric authentication locally on user devices to reduce latency and improve security compliance.

🔮 Future ImplicationsAI analysis grounded in cited sources

Consolidation of AI payment startups by traditional banking incumbents will accelerate by 2027.

Incumbents possess the necessary regulatory licenses and capital to absorb the high operational costs that currently stifle independent AI payment firms.

Standardization of AI auditability protocols will become a mandatory requirement for fintech licensing.

Regulators are increasingly demanding 'explainable AI' (XAI) to prevent discriminatory practices in automated credit and payment authorization systems.

⏳ Timeline

2023-05

Initial surge in venture capital funding for AI-driven payment infrastructure startups.

2024-09

First major regulatory warnings issued regarding AI-driven algorithmic bias in financial services.

2025-03

Major tech companies report lower-than-expected ROI on proprietary AI payment integration projects.

2026-02

Industry-wide shift toward hybrid AI-human verification models to address consumer trust issues.

📰

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

AI-curated news aggregator. All content rights belong to original publishers.

Original source: 钛媒体 ↗