🇨🇳cnBeta (Full RSS)•Stalecollected in 35m

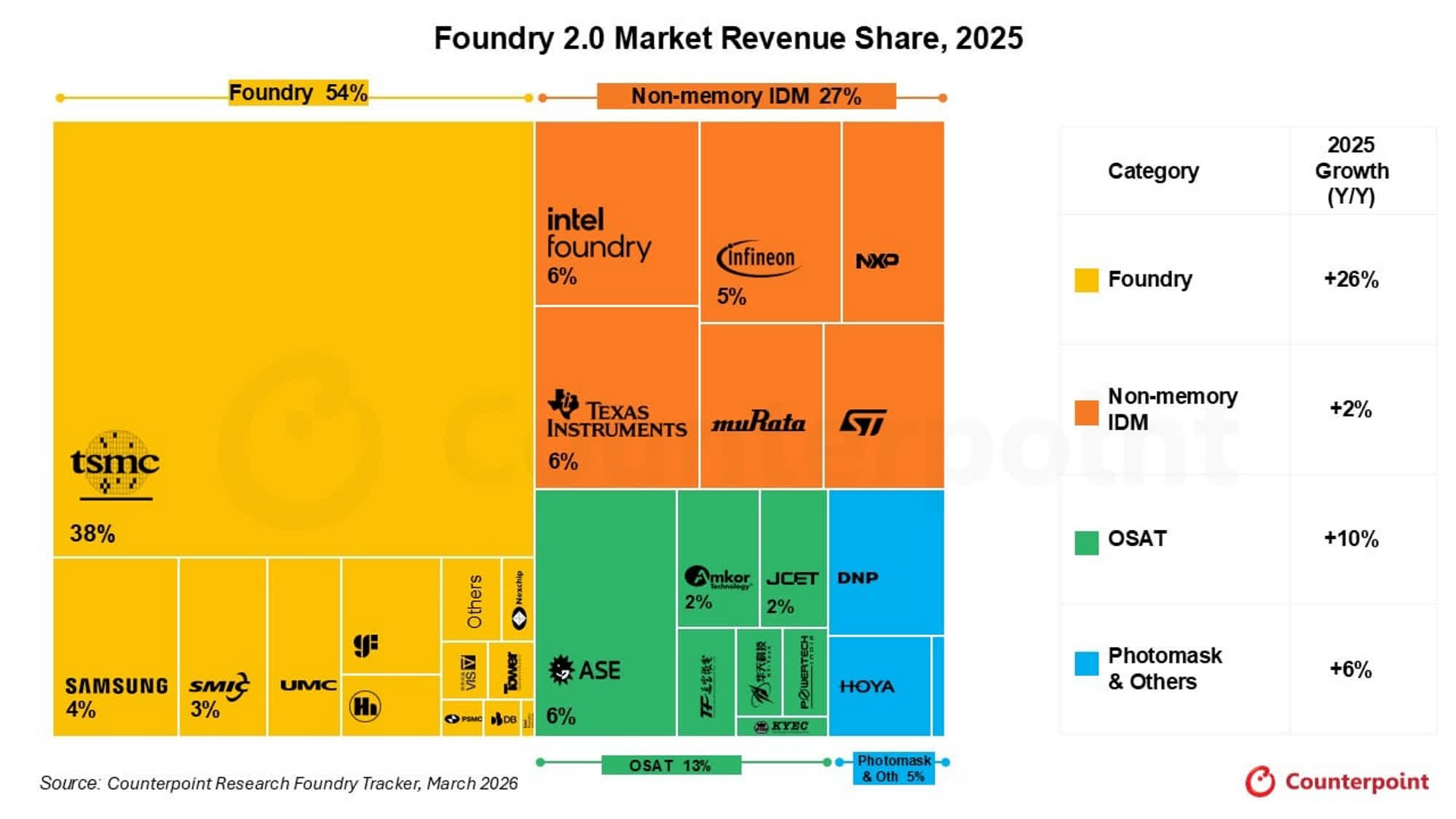

2025 Foundry Hits $320B on AI Surge

💡AI fuels $320B foundry boom—key for AI chip procurement strategy

⚡ 30-Second TL;DR

What Changed

2025 revenue reaches $320B, +16% YoY record high

Why It Matters

Signals robust AI hardware supply growth, easing chip shortages for AI training/inference. Boosts confidence in scaling AI infrastructure investments.

What To Do Next

Review Counterpoint's full Foundry 2.0 report for AI chip supply forecasts.

Who should care:Founders & Product Leaders

Key Points

- •2025 revenue reaches $320B, +16% YoY record high

- •AI accelerator chips as primary growth driver

- •'Foundry 2.0' describes evolved complex ecosystem

- •TSMC and major foundries secure huge profits

🧠 Deep Insight

AI-generated analysis for this event.

🔑 Enhanced Key Takeaways

- •The 'Foundry 2.0' framework emphasizes the shift from traditional wafer manufacturing to a comprehensive service model that integrates advanced packaging (CoWoS), silicon photonics, and heterogeneous chiplet integration.

- •Geopolitical diversification is a major component of the 2025 revenue surge, as foundries aggressively expanded capacity in the US, Japan, and Germany to mitigate supply chain risks associated with concentration in Taiwan.

- •The 16% YoY growth is heavily skewed toward sub-7nm process nodes, with 3nm and 2nm production capacity becoming the primary bottleneck and pricing premium driver for AI-focused hyperscalers.

📊 Competitor Analysis▸ Show

| Feature | TSMC | Samsung Foundry | Intel Foundry |

|---|---|---|---|

| Leading Node | 2nm (N2) | 2nm (SF2) | 18A |

| Advanced Packaging | CoWoS / SoIC | I-Cube / H-Cube | Foveros |

| AI Market Focus | High-performance GPU/ASIC | HBM-integrated logic | High-performance CPU/AI |

🛠️ Technical Deep Dive

- Shift to Gate-All-Around (GAA) transistor architectures at 2nm nodes to improve power efficiency and performance density for AI workloads.

- Adoption of backside power delivery networks (BSPDN) to reduce IR drop and signal interference in high-frequency AI accelerators.

- Expansion of Chip-on-Wafer-on-Substrate (CoWoS) capacity to address the critical HBM (High Bandwidth Memory) integration bottleneck for generative AI training chips.

🔮 Future ImplicationsAI analysis grounded in cited sources

Foundry capital expenditure will shift from pure lithography to advanced packaging infrastructure by 2027.

The physical limitations of monolithic die scaling necessitate multi-die chiplet architectures, making packaging the new primary performance bottleneck.

Regional foundry pricing will diverge significantly based on local subsidy structures.

The high operational costs of non-Taiwanese fabs are forcing foundries to pass on localized manufacturing premiums to customers seeking supply chain resilience.

⏳ Timeline

2022-12

TSMC begins mass production of 3nm (N3) process technology.

2023-08

TSMC announces massive expansion of CoWoS packaging capacity to meet surging AI demand.

2024-04

TSMC receives $6.6 billion in CHIPS Act funding for US-based advanced manufacturing.

2025-02

Foundry industry reports record-breaking quarterly revenue driven by AI accelerator shipments.

📰

Weekly AI Recap

Read this week's curated digest of top AI events →

👉Related Updates

Same topic

Explore #ai-chips

Same product

More on global-foundry-market

Same source

Latest from cnBeta (Full RSS)

Semiconductor stocks surge in A-share market opening

36氪•Jul 15

Driver Misuse of ADAS Poses Major Safety Risks

cnBeta (Full RSS)•Jul 15

ChatGPT Mac App Faces Privacy Backlash Over Local File Access

cnBeta (Full RSS)•Jul 14

Meta Sued Over AI-Driven Layoffs Alleging Disability Discrimination

cnBeta (Full RSS)•Jul 14

AI-curated news aggregator. All content rights belong to original publishers.

Original source: cnBeta (Full RSS) ↗